Enhanced integration of Empower LOS and DocMagic supports home equity, wholesale channels

Today, we're excited to post that Dark Matter Technologies (Dark Matter), an innovative new leader in mortgage technology backed by time-tested loan origination software and leadership, announced significant enhancements to the integration between the comprehensive Empower® loan origination system (LOS) and DocMagic’s document generation solution.

DocMagic, a leader in fully compliant loan document generation and comprehensive eMortgage services, debuted its native integration with the Empower system last year, making it seamless for retail mortgage lenders who use the Empower system to order initial and closing disclosures from DocMagic without having to build a custom connection. As a result of the latest enhancements to the integration, DocMagic services are now also available for wholesale and home equity originations in the Empower system.

“It’s really significant when two best-in-class vendors like Dark Matter and DocMagic integrate their products so customers no longer have to build out custom integrations — now it’s a true union,” said Rich Gagliano, Dark Matter Technologies’ chief executive officer. “We’re taking that value and convenience even further by bringing it to multiple origination channels.”

“We are thrilled to strengthen our collaboration with Dark Matter, offering top-tier documentation, compliance and eServices while also providing customers of the Empower system exceptional support backed by our award-winning customer service,” said DocMagic President and CEO Dominic Iannitti. "We look forward to continuing to integrate our two services further, supplying our proprietary ClickSign®, eNotary and Total eClose™ capabilities.”

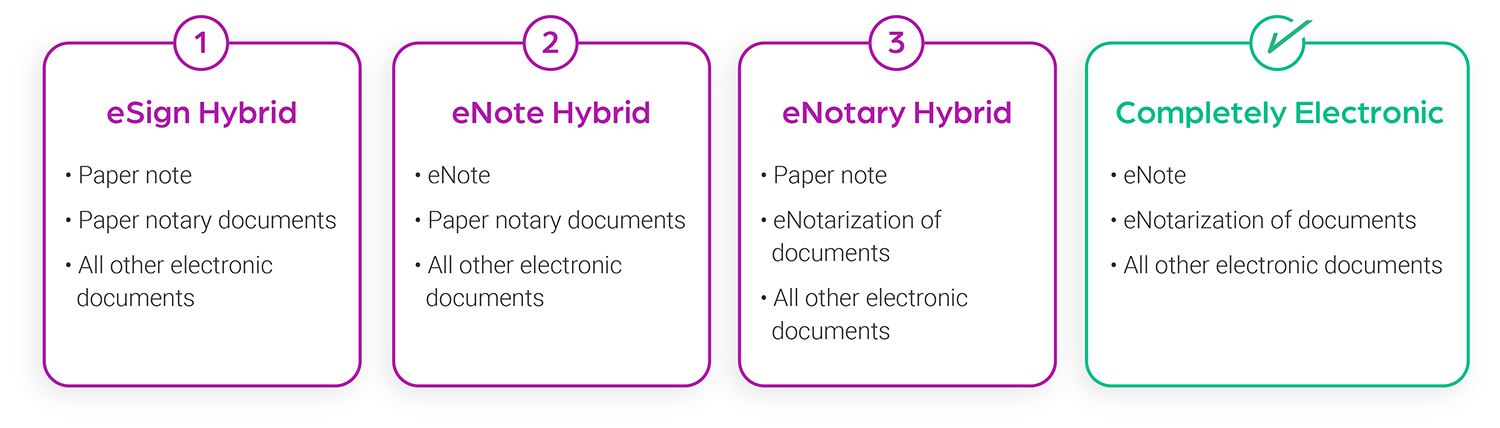

.jpg) Sommerville shares the reasons why lenders should consider the phased approach, and we delve into various

Sommerville shares the reasons why lenders should consider the phased approach, and we delve into various